The Modern DI Sales Playbook

Disability Income insurance (DI) is widely recognized as important but often feels complicated and easy to postpone. The key is framing -- when clients see the risk clearly, DI becomes obvious rather than awkward. This playbook teaches you how to:

- Start the DI conversation without triggering resistance

- Overcome client objections that usually derail the sale

- Make income protection feel relevant and actionable

Most clients have a monthly income that supports their lifestyle and various insurances (health, life, home, auto) to protect their assets. But, if they become too sick or hurt to work, health insurance covers medical bills and life insurance covers death, but nothing replaces lost income if they’re ever too sick or hurt to work.

Clients focus on protecting their lifestyle, family, and retirement—not buying DI. Your role is to protect the foundation of their plan. When you anticipate risks and help clients avoid financial chaos during a health crisis, you become a trusted advisor.

Start The Conversation

Avoid starting with "disability." Begin with an Income Protection Review:

"In our planning, we’ve discussed retirement planning, investments, and insurance. Next, I’d like to do a quick income protection review so we can confirm the plan holds up if you’re ever too sick or hurt to work." This approach:

- Sparks curiosity

- Frames income as an asset

- Avoids emotionally loaded language

Overcoming Client Objections

"We can manage without my income."

Clients may suggest downsizing, relying on a spouse’s income, or tapping retirement accounts.

Ask: Would they want to rely on these options while recovering from a serious illness? DI is about recovery with financial stability, not just survival. Show the long-term impact of income loss on retirement, lifestyle, and family security.

"I already have coverage through work."

Group disability insurance is a good start, but often insufficient:

- Benefits are usually taxable

- Caps restrict benefits, especially for higher earners

Bonuses and incentives typically aren’t covered Supplemental individual DI fills these gaps and protects more of what clients earn. Once limitations are clear, this objection usually disappears.

"I’m healthy and won’t get hurt."

Most long-term disability claims are due to illness, not injury. Majority stem from illnesses like cancer, cardiovascular disease, and musculoskeletal disorders

Make it personal by asking if they know someone who has battled a serious illness, or share a real story. Stories create clarity where statistics don’t.

Closing The Sale With OneProtection

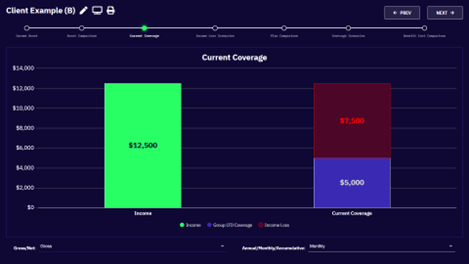

DI sales fail when clients can’t see the risk. OneProtection helps you:

- Visually explain income loss

- Address objections before they stall the sale

- Turn hesitation into action without pressure

Get Started Today

Visit https://one.oneprotection.tech/naifa to learn more and to schedule a one-on-one demo with Michael Sir, President and co-founder of OneProtection.